I defended my PhD in May 2016. Before embarking on my postdoc in Lebanon in November 2016, I spent a few months looking for jobs and working on publications (you can check the most recent ones here and here). Among these was one article that tells the main story of my PhD, and that I planned to submit to the journal Antipode. It tells the story of how a large amount of capital found its way into Lebanon’s real estate and banking sectors after the global financial crisis of 2008, constituting a direct and indirect “spatial fix,” a term by David Harvey that I’ve discussed before.

During my postdoc, I worked on a draft and submitted it in June 2017. Five months later, I got four peer reviews back, and the news that I should do major revisions. The peer reviews were quite helpful in getting the article into better shape, and even though I was self-employed by then, I spent many hours revising the article and getting it into shape. I resubmitted it at the end of April 2018.

In July, I got four more reviews back from the same reviewers. While they were very satisfied with the revisions, some wanted me to engage more with the theory. At this point, it had been over two years since I defended my PhD. I decided that I would no longer spend time on the article and retracted it after mulling over my options for a few months. The people at Antipode were very nice about it and I decided to publish the article on my blog, to make it freely available to everyone interested in the story of my PhD. Please download it here or read it below! Anyone who can spot an error gets a free copyedit (up to 5,000 words)! An author can’t do her own proofreading 🙂

The Spatial Fix in Lebanon:

Remittances, Petrodollars, and the Global Financial Crisis.

Dr. Marieke Krijnen, Editor | www.mariekekrijnen.com| info@mariekekrijnen.com

Abstract

From the early 2000s into the 2010s, Lebanon experienced a “spatial fix,” as surplus capital flowed towards the country and was invested in its built environment. This happened either directly, as investors and buyers invested in real estate; or indirectly, through housing and construction loans, provided by financial institutions who used surplus capital deposited with them. My findings offer three contributions to the theory of the spatial fix. First, we should diversify the origins and geographies of the capital flows involved in spatial fixes to include remittances of highly skilled expatriate workers as well as petrodollars. Second, the Lebanese case points to the widely diverging geographical consequences of financial crises and capital switches, demonstrating the importance of taking other kinds of financial systems into account. Finally, my findings reveal the crucial role of state institutions and connected elite interests in mediating and directing such capital flows.

Keywords: Lebanon, real estate, banking, financial crisis, spatial fix, mortgages.

Introduction

When real estate and mortgage markets collapsed across the globe in 2008, something remarkable happened in Lebanon: the country experienced its biggest real estate and banking boom in decades. Investment in real estate reached unprecedented heights between 2008 and 2012, despite the global financial crisis and regional political turmoil. In the nation’s capital Beirut, older buildings were emptied of their inhabitants and replaced with glitzy, luxurious, mostly residential high rises. At the same time, Lebanese domestic banks’ profits soared by 26.7 percent in 2008, and 37 percent in 2010, reaching US$1.6 billion (Bank Audi 2009; FFA Private Bank 2011). One could explain the urban transformation of Beirut and the upsurge in Lebanese banks’ profits by pointing to the apparent resilience of the country’s real estate and banking sectors in the face of regional conflict, or as yet another case of the rampant gentrification and neoliberal urban policy that has been plaguing the globe.

However, this does not tell us why so much capital flowed to Lebanon, where it came from, why it was invested in these particular sectors, and why during that particular moment in time. In this article, I show that the real estate and banking boom, which had already begun in the early 2000s, constituted a spatial fix for surplus capital of Gulf and Lebanese expatriate investors. A spatial fixoccurs when surplus capital is redirected towards other capital circuits or geographic regions where the profit rate is higher (Harvey 1978; Smith 1984). In Lebanon, this surplus capital consisted mostly of Lebanese expatriates’ remittances and petrodollars from the Arab Gulf countries. It found its way to Lebanon’s financial and real estate sectors as oil prices increased sharply, and these sectors remained unaffected by the consequences of the financial crisis. The spatial fix in Lebanon took place in two ways: directly, through the investment of surplus capital in real estate, and indirectly, as Lebanese banks invested the surplus capital, which had been deposited in their accounts, in housing and construction loans, propping up the real estate market and thus preserving the direct spatial fix. In this way, capital flows reaching Lebanon’s built environment played a role in negotiating and mediating the internal contradictions of the capitalist system, in particular those of today’s financialized economy.

The Lebanese case makes a number of contributions to the theory of the spatial fix. First, it forces us to diversify the nature of the capital flows involved, to include remittances by highly skilled Lebanese expatriate workers as well as petrodollars from Arab Gulf investors, so salient in the Middle East’s spatial fixes (Buckley and Hanieh 2014; Hanieh 2016; Bogaert 2018). Capital flowed towards Lebanon following previously carved-out paths and relationships with these investors. The nature of these flows also points towards a capital switch from the financial or “quaternary” circuit of capital to the secondary circuit of the built environment (Aalbers 2008; Harvey 1978). Second, the Lebanese story forces us to pay attention to the geographically differentiated consequences and impacts of financial crises. Countries with financial systems that remain unaffected by such crises can function as safe havens for fleeing capital (Kutz and Lenhardt 2016). Highly skilled expatriate workers living in crisis-stricken places engage in financial maneuvers that lead to booms in their country of origin. By pointing towards these dimensions, the article decenters narratives about the consequences of the 2008 financial crisis. Finally, my findings point towards the crucial role of the legal framework and state institutions, especially the Central Bank of Lebanon, in attracting and directing the capital flows that constitute the spatial fix, as well as the importance of financial institutions in mediating spatial fixes. Such actions can be explained when we dissect the political economy of Lebanon, which is dominated by an elite of real estate developers and bankers.

The arguments and data that I present here are derived from my longstanding research on Lebanon’s political economy and real estate market that began in 2008, included numerous interviews with real estate developers, bankers, residents, policymakers, lawyers, architects, economists, and other informants; the collection of dozens of property records, sales contracts, company data, laws and brochures; the surveying and mapping of urban change in a number of areas of Beirut; and an extensive review of business magazines and newspapers reporting on the real estate and financial sector in the country. In what follows, I will first tell the story of the real estate boom that started in the early 2000s and intensified after 2008, and show how this boom constituted a direct spatial fix for petrodollars as well as expatriate capital. Second, I show how after 2008, the surplus capital that had found its way to Lebanon’s unaffected banks in the form of deposits was switched into real estate via housing and construction loans, constituting another, indirect, spatial fix. Finally, I reflect on the contributions of my findings, outlined above.

A Direct Spatial Fix in a Time of Plenty: Lebanon’s Real Estate Boom 2000–2011

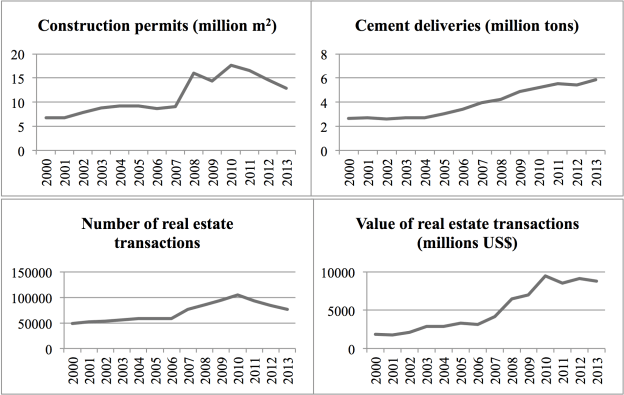

In the early 2000s, a real estate boom began to take shape in Lebanon. To get an idea of the scale of this boom, Figure 1 provides some indicators: cement deliveries, the number of construction permits and real estate transactions, as well as their value between 2000 and 2013. While none of these data are entirely reliable,[1] all figures show a pickup in growth that starts in the early 2000s, halts in 2006 after the Israeli war on Lebanon, and picks up again after 2007 to reach new heights after the global financial crisis of 2008.

Figure 1-Clockwise: Construction permits in million square meters (source); cement deliveries in tons (source, August 25, 2015); number and value of real estate transactions (source, August 25, 2015).

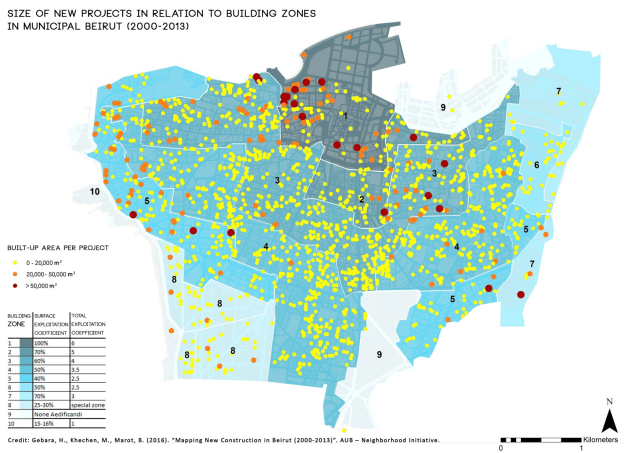

The unprecedented real estate boom resulted in countless new luxury apartments with an average size of 340 m2 (Wehbe 2014a), located in high-rise residential towers with their own water and electricity facilities (a necessity in a country where 24-hour service is mostly nonexistent, even in the capital), and amenities such as gyms and swimming pools, private security guards and driver rooms. Most of these apartments were sold off-plan, i.e. before construction even started, and financed in cash. As a result, the city is now dotted with a large number of towers that remain uninhabited for most of the year. In 2009, it was estimated that over 300 projects were under construction (Plus de 300 chantiers résidentiels à Beyrouth 2009). The high-end towers were concentrated mostly in the city center, along the seaside promenade in the west of the city, and in the traditionally upper middle-class area of Achrafieh (see Map 1). As a consequence of the construction boom, prices increased immensely in a very short period, quadrupling in areas popular with investors (Beirut ranks 52nd globally in house prices, 53rd in rental yield 2009; Global Property Guide 2011; Karam 2010; Krijnen 2010). As prices rose, investors moved from the initial core areas for luxury apartments to other areas where land prices were lower, and started to build smaller-sized apartments (Sakr 2013). The surge of investment in the city reverberated in other sectors as well, and some neighborhoods transformed into hubs for nightlife (Bonte 2016), hospitality, and arts and crafts. The increasingly trendy character of such areas, usually located further away from the centers of investment, was then used by real estate developers to market their projects as they moved there, leading to severe gentrification processes that are ongoing until this day (Krijnen and De Beukelaer 2015).

Map 1-Construction permits for large-scale projects and property prices in Beirut, 2000–2013 (Gebara et al. 2016). Used with written permission.

What lay behind this real estate boom and its timing? Who was investing in Lebanon’s real estate sector, and why? Where did all this capital come from? As I will show, most of the capital that flowed towards real estate during this boom came from Gulf investors and buyers, as well as Lebanese expatriate workers[2] (Halawi 2010; Hourani 2014; Krijnen 2010; The World Bank 2012) who had surplus capital to invest.[3] They “spatially fixed” this capital in Lebanon’s real estate sector, resulting in a large amount of structures that now house this money in their very form.

The concept of a spatial fix was first theorized by David Harvey (1978, 2001), to denote the switching of capital from the primary circuit of production into the secondary circuit of the built environment or to another geographical region. The reason for a spatial fix lies in the contradictions internal to the capitalist system, where competition between members of the capitalist class inevitably results in overaccumulation: an overproduction of goods or a surplus of profits for which insufficient profitable reinvestment options exist, risking devaluation. A strategy to prevent such a crisis of overaccumulation consists of “switching” the surplus capital from one capital circuit to another, or from one geographical region to another, to where the profit rate is higher. A spatial fix can be a temporary solution to a looming crisis of overaccumulation, which occurs when investors are left with a large glut of capital for which no profitable (or productive[4]) reinvestment exists. Indeed, it has been shown that just before a major financial crisis, investments in the built environment (i.e. spatial fixes) have generally peaked (Christophers 2011; Harvey 1978). In the case of Lebanon, a large amount of surplus capital came to the country and was spatially fixed. In what follows, I outline how and when petrodollars and expatriate capital found their way to Beirut’s real estate sector.

Surplus Capital: Petrodollars

During the early 2000s, oil prices rose sharply, reaching their peak in 2008. Consequently, investors from the Arab Gulf had large amounts of petrodollars at their disposal and were looking for profitable investment opportunities. Besides other Middle Eastern countries (Hanieh 2011; Bogaert 2018), they displayed a preference for Lebanon because of a longstanding historical relationship and a set of incentives provided by the Lebanese government.The latter passed a number of laws and regulations between 2000 and 2005 that attracted this surplus capital and encouraged its investment in real estate (Achkar 2011; Krijnen 2010; Krijnen and Fawaz 2010). These included a new building law that significantly increased the allowed built-up area, creating large rent gaps (Krijnen 2018); the easing of restrictions on foreign ownership of real estate; tax incentives to investors in tourism projects such as hotels and resorts; and finally, the loosening of Lebanese nationality requirements for companies registered in Lebanon.

Gulf investment in Lebanon’s real estate market was not new, but formed part of a longstanding historical relationship. During the early 1960s, Beirut was a booming financial center where Gulf Arabs came to recycle their petrodollars via the Euro-American banks headquartered there, supported by the Lebanese government. The latter had firmly set its sights on turning Beirut into a regional financial center after gaining independence in 1943 (Gates 1998). To this end, it had implemented a banking secrecy law in 1956, guaranteed the free mobility of capital and goods, stimulated tourism, legalized gambling, and provided infrastructure and low taxation incentives to investors (Gaspard 2004; Shwayri 2008). During this time, Lebanon also became a safe haven for Arab elites fleeing emerging postcolonial nationalist and socialist regimes (Nasr 1978). Both Gulf Arabs and fleeing Arab elites invested in Beirut’s real estate markets (Boudisseau 2001; Khalaf and Kongstadt 1973; Nasr 1978). The political-economic relationship between Lebanon and the Gulf States continued during the civil war (1975–1990),[5]when many Lebanese left the country to go work in the Gulf States following the oil boom of 1973. When the war was over, the reconstruction of Downtown Beirut by Lebanese businessman-turned-Prime Minister Rafiq Hariri attracted Gulf capital as well. Hariri was a dual Lebanese-Saudi Arabian citizen who had amassed a fortune working in construction in Saudi Arabia during the war. He used his contacts to channel capital towards Lebanon and kept close relations with Saudi investors (Baumann 2016; Hourani 2013).

Encouraged by these preexisting connections and relationships and the legal changes between 2000–2005, investments from the Arab Gulf countries increased massively. Foreign direct investment in Lebanon grew forty percent annually from 2002 to reach US$2.5 billion in 2006, sixty percent of which was invested in real estate, mainly by investors from Saudi Arabia, Kuwait, and the United Arab Emirates (Credit Libanais 2008). These were mostly private investors and investment companies with close connections to ruling elites (Hanieh 2011; Hertog 2007). While a part of these petrodollars went to private apartments, most went into real estate development itself. The financial crisis coincided with the peak in oil prices in 2008. While the crisis did not leave the Gulf unaffected (Bassens 2013), plenty of surplus capital was still available. Since Lebanon’s economy had escaped the crisis, the flow of petrodollars intensified (Global Property Guide 2011). Investors were also encouraged by the resolution of a political standoff that had escalated violently in May 2008, and ended in a peace agreement signed in Qatar, after which a new national-unity government was installed.

Gulf investors focused mostly on large-scale luxury resorts and residential towers, including the Four Seasons Hotel on the Downtown seafront, developed by the Saudi Kingdom Holding and the residential Clemenceau Tower west of Downtown, owned by Kuwaiti Gulfinvest International. Other investors include the Emirati Abu Dhabi Investment House and the Kuwaiti Al Taameer Real Estate Investment Company, who both bought and developed a number of plots in Downtown Beirut, including the Ramada Hotel (Krijnen 2010). Apartment buyers from the Gulf, while more numerous before the 2008 boom, still bought a significant amount of the most expensive, luxurious apartments with surface areas of a few hundred square meters each. Examples include the Nova Towers in Qoreitem, with 600 m2 apartments, and Bahri Gardens 2 in Raouche, with 650 m2 apartments.

Surplus Capital: Lebanese Expatriate Investors

In the early 2000s, Lebanese expatriates, many of whom were employed in the Gulf, experienced financial windfalls due to the rising oil prices. These were often spent on purchasing a home in their country of origin. Expatriates in other parts of the world profited from the generally fast-growing tertiary economies that employed them (De Bel-Air 2017). Many of these expatriates started to invest in a second home in their homeland, or got involved in financing real estate projects. Expatriates have bought and constructed houses during their annual return to the motherland for decades (Labaki 2006). But around the early 2000s, their focus shifted increasingly towards purchasing apartments in or around Beirut.

When the crisis hit in 2008, especially after the downturn in Dubai’s property markets and financial sector (BlomInvest Bank 2010), these expatriates intensified their investments. They took capital from places where the economy had tanked and invested it in at homeland. The real estate market in Beirut, with its incentives and facilities, its optimistic political security situation after the peace agreement of 2008, and its promise of a home in the homeland, provided a favorable outlet for this surplus capital. They “started to put their money in real property,” seeing that the market in Beirut was stable, as opposed to the markets of the countries where they were living[6] (Wehbe 2014c). It is estimated that in 2010, forty to forty-five percent of demand for residential real estate came from Lebanese expatriates, mostly for high-end apartments. Real estate agents and developers actively tried to reach these clients (Pearlman 2014), through online real estate portals and roadshows.[7] Expatriates bought an apartment as a retirement home, a summer residence or for their children. They would often deposit a down payment and pay the rest of the sum in subsequent installments, usually following different stages of completion of the building. These buyers relied mostly on personal savings, mortgages, and assistance from family members, including expatriates (Krijnen and De Beukelaer 2015).

Lebanese expatriate investors did not only buy apartments, but went into real estate development as well. They focused mostly on residential developments. An example is the AYA-tower by HAR-properties, located in Mar Mikhael. HAR’S CEO Fahed Hariri is a billionaire heir of the late Prime Minister who made his fortune in the Gulf, has resided in Dubai and currently resides in Paris (Krijnen and De Beukelaer 2015). Another example is the Trillium Tower by Mercury Development, now called Trillium Development, a company founded by Lebanese-British entrepreneur Mustapha Ahmad. Before coming to Beirut, Mercury made a fortune by working in postwar reconstruction in Afghanistan and Iraq.[8] Buyers for this project consisted of sixty percent expats and ten percent foreigners (Boudisseau 2011). Hence, Lebanese real estate developers were often connected to transnational capital flows and increasingly took their money to Beirut. These developers were, for the most part, larger holding companies that would create special-purpose vehicles (SPVs) to finance their projects. They were different from the smaller, family-based developers that characterized Lebanese real estate development earlier. They viewed themselves as more professional, more financially literate, and able to execute larger-scale projects. To set themselves apart, they ignored the existing Building Promoters Federation Lebanon and created their own association, REDAL, which seeks to promote modern financing tools and market transparency.[9]

In short, in the early 2000s, Gulf and Lebanese expatriate investors took their money to what they perceived to be a profitable market, “switching” surplus capital into the real estate sector. This spatial fix intensified when Lebanon became a safe haven during the financial crisis and they could no longer invest their capital as profitably in the collapsing European and Gulf real estate markets (Karam 2010; McGinley 2010). According to insiders, there was a “momentum” after the 2008 peace agreement, and the previous increase in prices completely escalated.[10] However, around 2011, a change in the real estate market led to a change in the direction of the spatial fix. This was caused by the highly inflated prices of real estate and land, an oversupply of luxury apartments, and the increasing political insecurity following the Arab uprisings. The revolution in Syria had caused a deep rift between Lebanon’s political factions. While many wealthy Syrians helped prop up the real estate market when they fled to Lebanon and purchased or rented luxury apartments (Ashkar 2015), in a climate of increasing insecurity and stagnation, the spatial fix took on a new form.

An Indirect Spatial Fix in a Time of Stagnation: Mortgage Markets in Lebanon 2008–2016

The 2000s Banking Boom

In order to understand the new form that the spatial fix took at this time, we have to understand that there was not just a real estate, but also a banking boom in the early 2000s. Lebanese banks had managed to attract a large amount of deposits because of their favorable position in the country and the region. Back in the 1960s, when Beirut was still a regional financial center, Euro-American banks had dominated the financial sector. When these left during the civil war however, Lebanese banks moved into a monopoly position, aided by the Free Banking Law of 1977, which lifted some of the restrictions placed on opening new banks in the country (NB Hourani 2010). At the same time, and following the oil boom of 1973, a large number of Lebanese immigrated to the Gulf (Kubursi 1999), significantly increasing the amount of remittances flowing to Lebanon and filling the coffers of the newly established banks. Since the government could not collect sufficient taxes due to the war, it started to rely on loans provided by these domestic banks in order to continue to fulfill its basic duties (Kubursi 1999). This trend continued after the war ended in 1990, and in fact increased massively as reconstruction got underway. Public debt stood at 190 percent of GDP in 2008 (Traboulsi 2014).

While this constituted a precarious model of public financing, as bailouts and donor conferences throughout the years reveal, the banks profited greatly from this model. The continued emigration of the Lebanese guaranteed a steady flow of income in the form of remittances (Labaki 2006), and the high interest rates that the government paid over its loans (Dibeh 2011) ensured that the banks did not look for other investment opportunities. Indeed, the Central Bank had forbidden them from investing in the speculative financial products popular at the time, which ultimately led to the downfall of financial institutions.[11] When the financial crisis began to spread around the globe in 2008 therefore, Lebanon’s banks remained unaffected.

The Post-2008 Banking Boom

Investors paid heed, and started to transfer their money to Lebanon’s banks in large amounts, seeing that the banks remained unaffected and could offer a higher interest rate than banks in their countries of residence, in addition to banking secrecy and a tax exemption on non-resident deposits (BlomInvest Bank 2010; Hourani 2009; Khoury and Kanj 2013). While the origins of these capital flows cannot be determined in definite terms because of Lebanon’s banking secrecy,[12] all indicators point towards a significant role for Lebanese expatriates and Gulf investors, as during the real estate boom. Expatriates are traditionally a loyal bank client with a high degree of trust in the banking sector, who either deposit their savings or use the accounts for remittances to their families (Berthélemy et al. 2007; Finger and Hesse 2009; Hardie 2012; Labaki 2006). Most funds are transferred from the Gulf States and West Africa (Awdeh 2013; Brand 2007; G Hourani 2010), and Europe, North America and other parts of Africa (Khoury and Kanj 2013). As the Vice President of an economic think tank explained: “The Lebanese diaspora (…) realized that Lebanon was a safer environment for their money, so the money came in.”[13] An anecdote told by the Central Bank’s governor himself relates how a rich Lebanese investor living overseas called him after the collapse of Lehman Brothers in the US: “He was always skeptical about the stability here. But he told me, ‘I sent all my money to Beirut now to the banks. You were right’” (Daragahi 2009). Lebanese banks have actively tried to attract these non-resident deposits via their websites, by sending officers abroad or via their offices in countries with large expatriate Lebanese populations (Pearlman 2014).

Another significant part of bank transfers came from Gulf residents. These increased in 2008, when the financial crisis did not spare their region (Kanj and Khoury 2013). Because of the earlier-mentioned banking secrecy, precise numbers on Gulf deposits are hard to obtain, however, and, as mentioned above, it is impossible to gauge the amount of illicit wealth that is stored in Lebanese bank accounts. An economy professor stated: “I suspect the big accounts are affiliated with money laundering, illicit activities and Gulf money, petrodollars.”[14] As confirmed by a finance journalist, Gulf investors also bought shares of Lebanese banks if their funds were sufficient.[15] A look at the Almanac of Lebanese banks confirms this: of 34 banks, I found thirteen with shareholders from the Gulf, eleven of which have Saudi shareholders. Hanieh (2011:157) names other examples of major Gulf shareholders in Lebanese banks.

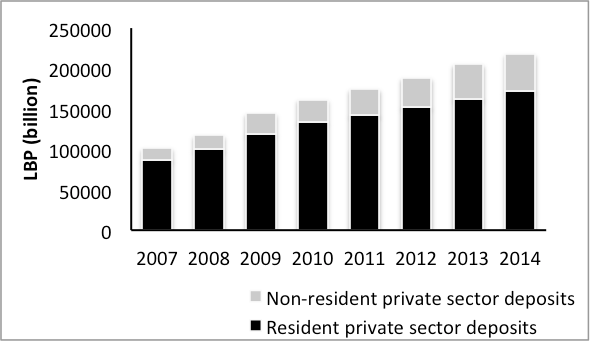

Although the exact numbers remain unknown, it is safe to assume that remittances and transfers from Lebanese expatriates and Gulf residents are mainly responsible for the increase in resident as well as non-resident deposits in Lebanon’s domestic banks after 2008. Deposits grew by fifteen percent in 2008, twenty-two percent in 2009 and nine percent in 2011, with bank assets at US$176 billion, a stunning 350 percent of Lebanon’s GDP, in 2014 (Chaaban 2016; Wehbe 2014b). Banks’ net profits increased by twenty-six percent in 2008 (Bank Audi 2014a) and reached $1.6 billion in 2013 (Wehbe 2014b). Meanwhile, non-resident deposits increased by forty-four percent in 2009 (Association of Banks in Lebanon 2009), and in 2013 constituted nearly twenty-three percent of all deposits, from ten percent in 1997 (Khoury and Kanj 2013: 154). Figure 2 shows the growth in both resident and non-resident deposits for the period 2007–2014.

Figure 2-Increase in total deposits of the resident and non-resident private sector in Lebanese pounds. December of each year, source.

An Indirect Spatial Fix

The large amount of excess liquidity that resulted from this increase in deposits had to be profitably reinvested somewhere. From this moment on, the Central Bank began to encourage banks to invest these surpluses in consumer credit, including mortgages and construction loans. The role of the Central Bank was crucial, as an institution controlling the production of money and governing the relations between the different circuits of capital, including the switching of capital into the built environment (Harvey 1978). It decided to step in at this point because first, after the large influx of capital following the global financial meltdown and the (temporary) resolution of Lebanon’s political crisis, the real estate boom had driven up land and apartment prices to such an extent that the majority of people looking for housing in Beirut could not afford to buy or rent anything. Second, banks’ returns from investments in government bonds had been declining since a series of bailouts and debt rollovers (Sadikov et al. 2012; Srouji 2005). The rollover of the public debt and subsequent lowering of interest rates had left the banks looking for other investment options. At this juncture, the Central Bank intervened.

While the Central Bank’s intervention was relatively modest at first, it increased significantly around 2011, as the real estate market in Beirut had begun to stagnate, with sales transactions and foreign and expatriate demand slowing down significantly in 2011–2012 (Bank Audi 2014b; Hourani 2009; Nash 2014; Sakr 2013). Gulf investment decreased, following declining oil prices and intergovernmental conflicts related to the uprising in Syria (Abou-Mosleh 2015; Hourani 2014). The stagnation exacerbated as a series of bomb attacks and political rifts plunged the country into political insecurity. Over 200,000 apartments were sitting unsold on the market as of June 2014 (Wehbe 2014c). Some real estate developers in fact canceled their projects.[16] Meanwhile, expatriate deposits kept flowing in, not much influenced by the dire political situation (Khoury and Kanj 2013), and the continuing rolling over of the debt had lowered interest rates on government bonds to a little over five percent for twelve-month treasury bills in 2013.[17] In order to prevent a crisis and subsequent devaluation of assets, and provide an option for local Lebanese excluded from the real estate market, excess liquidity was directed towards the built environment by incentivizing banks to invest in housing and construction loans. In this way, renewed demand could compensate for falling sales rates as the real estate boom stagnated, while capital kept circulating profitably (cf. Aalbers and Christophers 2014) and a collapse of the real estate market was prevented. As an economic researcher at a banking association stated, this intervention “removed extra liquidity” from the system and “channeled it for investment.”[18] Hence, surplus capital found its way to Lebanon’s real estate sector via housing and construction loans (note that banks are explicitly forbidden from engaging in real estate development directly).

How did the Central Bank achieve this spatial fix? Traditionally, credit has played a very minor role as a means of obtaining housing or land in Lebanon: buyers usually paid in installments (Bou Akar 2012; Fawaz 2009; Peters et al. 2004) or relied on personal funds, and developers made deals with landowners, given them apartments in exchange. The Central Bank first actively incentivized mortgage loans through reducing its reserve requirements in June 2009 (Sakr 2013) and permitting under-construction loans, which were especially targeted towards expatriates not needing to move in directly (Bathish 2012). As a result, lending to non-residents increased rapidly (Sadikov et al. 2012). Moreover, the ceiling to apply for a public housing loan through the Public Corporation for Housing (PCH) was raised, as well as the loan-to-value ratio (from 60 to 80 percent of the house price). Second, in 2011, when the real estate market started showing signs of stagnation, the Central Bank rolled out yet another incentives package, geared towards ensuring continuing liquidity for developers and subsidizing mortgage interest rates for resident Lebanese, given stagnated diaspora demand. When banks had used the maximum allowed percentage of their reserve requirements, the Central Bank intervened once again. In January 2013, it provided the commercial banks with one-percent-interest loans at a total value of US$1.46 billion, in order to stimulate credit provision to the housing sector (Sakr 2013), aimed at apartments in the lower middle segment. The banks welcomed this intervention with great enthusiasm; some of them offered the first loans within two days (Schellen 2013). At the same time, the PCH received funds to start offering more loans in conjunction with the commercial banks, at subsidized interest rates (Habib 2014; Schellen 2013). Hence, banks diversified their investments, focusing less on government debt and more on private credit, especially housing and construction loans (Saad 2014; Wehbe 2014b). Table 1outlines the most important regulations and incentives issued by the Central Bank since 2009.

| Date | Reform | Content |

| Jun. 2009 | Intermediate Circulars 185/186/191/197/198/210 Intermediate Decision 10187 | -Exempting banks from reserve requirements on certain loans including most housing loans, allowing banks to deduct 60 to 100 percent of a qualifying loan from required reserves on customer deposits, up to a ceiling of seventy-five percent of the reserve requirement for all qualifying loans, including mortgages. -Zero-interest rate. -Valid for loans granted from January 1, 2009, until June 30, 2011. -These loans are meant to finance new projects or extend existing projects or for the purchasing of a new main residence, and should not be for consumptive, real estate development and operational capital purposes. |

| Jan. 2010 | Intermediate Circular 213 | -Banks can use up to 90 percent of reserve requirements for the exemptions passed in 2009. -Loans granted through the agreement with the Public Corporation for Housing can be deducted for up to 80 percent, not 60 percent. |

| Jan. 2011 | Intermediate Circular 243 | -Allowing banks to use up to 90 percent of their reserve requirements for housing loans. |

| Jan. 14, 2013 | Intermediate Decision 11329/Intermediate Circular 313, adding Art. 9-bis to Basic Decision 6116 (March 7, 1996). | -Providing commercial banks with 2.2 trillion LBP (US$1.46 billion) credit at 1 percent interest rate until December 31, 2013. -50 percent of this is to be used for housing loans -Ceiling on loan is LBP800 million (US$530,300) -Maximum interest rate is 5.44 percent based on one-year Treasury Bills -Down payment is obligatory -Loan cannot be combined with other bank loans. -The Housing Bank may benefit from 80 billion Lebanese pounds in credit at a 1 percent interest provided interests and commissions on loans granted to customers do not exceed 3 percent. |

Table 1-Central Bank mortgage regulations and incentives. Based on Schellen (2013), Sakr (2013), and several circulars from the Central Bank of Lebanon, source, also obtained during interviews in December 2013 and October 2014.

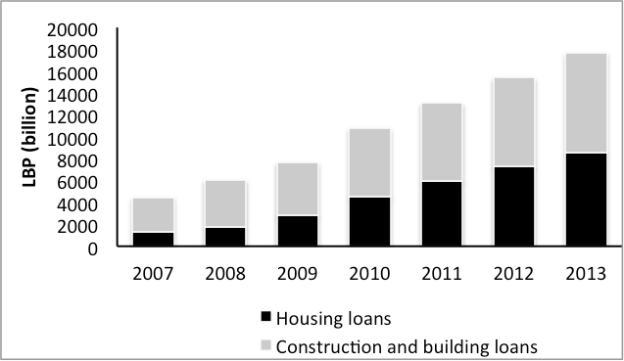

In summary, the Central Bank first stepped in in 2009, responding mostly to banks’ enormous excess liquidity due to the inflow of deposits, and significantly increased its intervention when the real estate market stagnated in 2011, to stimulate the real estate sector in the interests of developers and other people dependent on this sector (Schellen 2013). An unprecedented mortgage boom ensued. From 2008 to 2010, private credit grew at twenty percent per year, compared to an average six percent during 2005–2007. Consequently, the number and amount of mortgages has increased (Sadikov et al. 2012). Loans benefiting from the 2009 exemptions grew fast, and housing loans even faster. Construction loans increased by twelve percent in 2009 and thirty percent in 2010; housing loans increased by thirty-four percent in 2008, fifty-nine percent in 2009 and even sixty-one percent (!) in 2010 (Bank Audi 2010). They continued to grow steadily into 2013 (see Figure 3). According to a board member of real estate developers association REDAL, about half of clients now finance their purchase with a mortgage,[19] and various online mortgage comparison portals have sprung up catering to resident and expatriate Lebanese alike[20] (Bathish 2012; Cauli 2014).

Figure 3-Housing and construction loans to the resident private sector, 2007–2013, in billion Lebanese pounds(Bank Audi 2010, 2015).

Conclusion

In this article, I have shown that the real estate and mortgage booms in Lebanon constituted a spatial fix for surplus capital that was channeled towards the country by Lebanese expatriates and Gulf investors. The spatial fix occurred in a direct manner, through investment in real estate development, and an indirect manner, through housing and construction loans. It kept Lebanon’s political economy, dependent on domestic public debt, real estate, and remittances, afloat. It also kept capital circulating, alleviating overaccumulation in the banks. The role of petrodollars from the Gulf, Lebanese expatriates and the Central Bank proved to be crucial in this set-up. Several contributions can be gleaned from my findings.

First, they point towards the importance of diversifying capital flows that are involved in spatial fixes, to include remittances from (highly skilled) expatriate worker populations and petrodollars from the Gulf. The expatriate transfers and investments that shore up Lebanon’s political economy (Johnson 2017; Krijnen et al. 2017) played several roles in the spatial fix: expatriates bought real estate, but also invested in its development. They deposited money in the banks, but also took out loans to finance apartment purchases.This role for expatriate capital can be found in other countries in the Global South too (Grant 2007; Wu 2000), and should be taken into account when studying spatial fixes. Gulf capital played an important role in Lebanon’s spatial fix as well, as large amounts were invested in its real estate and banking sector. This not only had a profound impact on the built environment of Beirut, but also on Lebanon’s political economy. The banks ran into considerable excess liquidity that they could put to profitable use via government loans and, later, housing and construction loans. The economies of Lebanon and some Gulf countries partially reproduced each other (Hanieh 2011), as Gulf investors deposited their funds and bought shares in Lebanon’s banks, and helped bail out Lebanon’s economy during public debt and other crises via several Paris conferences. The size of their investments in Lebanon made the country “too important to fail.” Gulf capital was spatially fixed in other Middle Eastern countries as well (Barthel 2010; Bogaert 2018; Daher 2008; Musa 2013; Simpson 2013) and continues to play an important role in the creation of spatial fixes (Hanieh 2016). Hence, the role of expatriate remittances and petrodollars in spatial fixes across the globe deserves closer scrutiny.

The kinds of capital flows and investors involved carry some implications for the theory of the spatial fix itself. The post-2008 spatial fix in Lebanon was a geographical phenomenon, with capital moving towards the country from other contexts, and not a response to falling profit rates in the industrial sector (Harvey 1978; Smith 1986). However, real estate markets provide a favorable environment for capital switching not necessarily induced by falling rates of profit (see Charney 2001 and Wyly et al. 2004). In this case, we could argue that part of Lebanon’s spatial fix was a capital switch from the quaternary circuit of finance to the secondary circuit of the built environment, something usually theorized the other way around (Aalbers 2008; Silver 2003[21]). Some revenues transferred to Lebanon were part of the quaternary circuit, because many Lebanese expatriates work in financial sectors and centers such as the City of London (Krijnen et al. 2017). On the other hand, petrodollars constitute “ready-made” overaccumulated capital,[22] deriving from a primary circuit but also constituting a monopoly rent (Harvey 2010:83). This points towards other directionalities and origins of surplus capital than commonly theorized.

Second, my findings show that the global financial crisis was not so much a crisis on a global scale, as it was the instigator of a geographically differentiated capital switch that created booms and busts around the globe. This decenters dominant geographical narratives of the crisis and points towards the importance of taking other kinds of financial systems, with different levels of connectivity to the global financial system, into account when studying political economies across the globe (cf. Kutz and Lenhardt 2016). In Lebanon’s case, domestically held public debt played an important role in avoiding the consequences of the crisis (Hardie 2012) and indeed profiting from it. The high interest rates on government loans provided a steady source of income for the banks, who did not have to resort to risky financial products in search of a good rate of return. The post-2008 real estate and banking booms became possible because of this set-up. As the shocks of the financial crisis reverberated across the globe, Lebanon’s unaffected financial and real estate markets and beaming political confidence provided the perfect escape for crisis-haunted investors looking to take their money elsewhere. Lebanon’s highly skilled expatriate population and Gulf investors played a crucial role in this capital switch (Krijnen et al. 2017).They chose Lebanon for personal, business, relational, and socio-cultural reasons. In this way, capital “landed” in Beirut in a specific, highly transnational way (see Rouanet and Halbert 2014). Such “personal” safe havens arguably play important roles in the global financial system, and should be taken into account when understanding the geographical consequences of financial crises.

Third, the spatial fix was created through state interventions in the legal and institutional framework, with a crucial role for the Central Bank. This is not a coincidence. At any point during a capital switch or spatial fix, the existing legal framework and political-economic model of government in a country is crucial in swaying investors’ decisions (see also Krijnen 2018). Lebanon decided to become a financial center back in the 1950s. The state passed laws that attracted capital to its real estate and banking sectors, and did the same in the 2000s. These are political choices, and they were made in the interests of a ruling elite with overlapping interests in real estate, banking, and politics (Chaaban 2016; Krijnen 2016). The Central Bank-provided mortgage incentives ensured a profitable reinvestment of overaccumulated banking deposits and maintained high housing prices, while forcing the Lebanese middle class to get into debt and pay monthly interest rates to the banks. Meanwhile, no housing policy exists for the lower classes, for which even the subsidized loans provided through the Public Corporation for Housing remain unaffordable (UN-Habitat and UNHCR 2014). Together with plans to liberalize the last rent-controlled units in the country (Marot 2014), prospects for Lebanon’s poor and disenfranchised are bleak indeed, as the state intervenes only to protect the interests of politicians involved in its banking and real estate sectors. The mortgage-based spatial fix leads to more inequality (see also Wyly et al. 2004). We should therefore not forget that “the capitalist system” might indeed put us before some contradictions that are hard to solve, but at the same time, that it is governments’ political choices, made in the interests of ruling elites, that push capital in certain directions, which might exacerbate said contradictions.

To conclude, the spatial fix in Lebanon has long-term implications for the stability of its political-economic system. The switching of expatriate and Gulf capital into the built environment played an important role in mediating the contradictions of the capitalist system, creating a spatial fix, i.e. a temporary displacement of overaccumulated capital. However, such displacement only serves to exacerbate the contradictions of capitalism (Harvey 1978). In the United States for example, the propping up of the real estate sector and its function as a valve to relieve overaccumulation was only temporary and ultimately, the resulting crisis was even more severe (Gotham 2009). As the Lebanese case shows, a glut of money in the Global South is now potentially reproducing the same problematic conjuncture of capital switching into the built environment to temporarily relieve crises of overaccumulation. It remains to be seen whether a similar mechanism will occur in Lebanon, not in the least because of the Central Bank’s conservative regulation of the mortgage market. However, in the absence of any public housing provision, and unless the reconstruction of Syria begins soon or significant steps are taken to exploit the country’s offshore gas and oil reserves, the growth of (state-subsidized) mortgage loans is the only way in which the (lower) middle class can access housing and Lebanon is able to continue its real estate and banking-based economic growth.

Acknowledgements

I thank four anonymous peer reviewers for their time and helpful suggestions, and Antipode’s editor Dr. Nik Theodore and Editorial Office Manager Andy Kent for their help and patience.

References

Aalbers MB (2008) The financialization of home and the mortgage market crisis. Competition & Change12(2):148–166

Aalbers MB and Christophers B (2014) Centring housing in political economy. Housing, Theory and Society31(4):373–394

Abou-Mosleh F (2015) Lebanon’s economic dependence on the Gulf: Debunking the myths. Al Akhbar English23 February

Achkar H (2011) The role of the state in initiating gentrification: The case of the neighborhood of Achrafieh in Beirut. MA-thesis, Lebanese University

Ashkar H (2015) Benefiting from a crisis: Lebanese upscale real-estate industry and the war in Syria. Confluences Mediterranée92(1):89–100

Association of Banks in Lebanon (2009) Part Four. Activity and Performance of the Lebanese Banking Sector in 2009. Beirut: Association of Banks in Lebanon

Awdeh A (2013) Remittances to Lebanon: Economic Impact and the Role of Banks. Working Paper, UN-ESCWA, Strengthening Capacities to Utilize Workers’ Remittances for Development Workshop

Bank Audi (2009) Lebanon Banking Sector Report. Beirut: Bank Audi

Bank Audi (2010) Lebanon Real Estate Report. Beirut: Bank Audi

Bank Audi (2014a) Lebanon Banking Sector Report. Beirut: Bank Audi

Bank Audi (2014b) Lebanon Real Estate Report. Beirut: Bank Audi

Bank Audi (2015) Lebanon Real Estate Sector: A Weakening Demand in a Buyer’s Market.Beirut: Bank Audi

Barthel P-A (2010) Arab mega-projects: Between the Dubai effect, global crisis, social mobilization and a sustainable shift. Built Environment36(2):133–145

Bassens D (2013) The economic and financial dimensions. In M Acuto and W Steele (eds) Global City Challenges: Debating a Concept, Improving the Practice (pp 47–62). Houndmills and New York: Palgrave Macmillan

Bathish H (2012) Housing loans… Banks love ’em. November issue, Bold Magazine

Baumann H (2016) Citizen Hariri. Lebanon’s Neoliberal Reconstruction. Oxford and New York: Oxford University Press

“Beirut ranks 52nd globally in house prices, 53rd in rental yield” (2009) The Daily Star, 22 December

Berthélemy J-C, Dessus S and Nahas C (2007) Exploring Lebanon’s growth prospects. Policy Research Working Paper 4332, World Bank

BlomInvest Bank (2010) Lebanese Real Estate: A Safe Haven. A Decade of Real Estate Demand in Lebanon. Beirut: BlomInvest Bank

Bogaert K (2018) Globalized Authoritarianism: Megaprojects, Slums, and Class Relations in Urban Morocco. Minneapolis: University of Minnesota Press

Bonte M (2016) Eat, drink and be merry, for tomorrow we die. Alcohol practices in Mar Mikhael, Beirut. In T Thurnell-Read (ed) Drinking Dilemmas: Space, Culture and Identity(pp 81–98). London and New York: Routledge

Bou Akar H (2005) Displacement, politics and governance: Access to low-income housing in a Beirut suburb. MA-thesis, Massachusetts Institute of Technology

Bou Akar H (2012) Contesting Beirut’s frontiers. City & Society24(2):150–172

Boudisseau G (2001) Espaces commerciaux, centralités et logiques d’acteurs a Beyrouth: Le cas de Hamra et de Verdun. PhD-thesis, Université François-Rabelais de Tours

Boudisseau G (2011) Interview Trillium Beirut. April issue, Le Commerce du Levant

Brand LA (2007) State, citizenship, and diaspora: The cases of Jordan and Lebanon.Working Paper 146, School of International Relations, University of California San Diego

Buckley M and Hanieh A (2014) Diversification by urbanization: Tracing the property-finance nexus in Dubai and the Gulf. International Journal of Urban and Regional Research, 38(1):155–175

Cauli T (2014) Properties a click away. Does the internet help or hinder buyers in Lebanon’s real estate market? April issue, The Executive

Chaaban J (2016) I’ve got the power: Mapping connections between Lebanon’s banking sector and the ruling class.Working paper No. 1059. Cairo: Economic Research Forum

Charney I (2001) Three dimensions of capital switching within the real estate sector: A Canadian case study. International Journal of Urban and Regional Research25(4):740–758

Christophers B (2011) Revisiting the urbanization of capital. Annals of the Association of American Geographers101(6):1347–1364

Credit Libanais (2008) The Lebanese Real Estate Sector. Beirut: Crédit Libanais

Daher RF (2008) Amman: Disguised genealogy and recent urban restructuring and neoliberal threats. In: Y Elsheshtawy Y (ed) The Evolving Arab City: Tradition, Modernity and Urban Development (pp 37–68). London: Routledge

Daragahi B (2009) Lebanon Central Bank chief got it right. Los Angeles Times21 February

De Bel-Air F (2017) Migration Profile: Lebanon(Policy Brief No. 12). Florence: European University Institute.

Dibeh G (2011) The political economy of stabilisation in post-war Lebanon. In D Cobham D and G Dibeh (eds) Money in the Middle East and North Africa: Monetary Policy Frameworks and Strategies (pp 37–59).London and New York: Routledge

Dillman B (2007) Introduction: Shining light on the shadows: The political economy of illicit transactions in the Mediterranean. Mediterranean Politics12(2):123–139

Fawaz M (2009) Contracts and retaliation: Securing housing exchanges in the interstice of the formal/informal Beirut (Lebanon) housing market. Journal of Planning Education and Research29(1):90–107

Fernandez R and Aalbers MB (2016) Financialization and housing: Between globalization and Varieties of Capitalism. Competition & Change20(2):71–88

Fernandez R, Hofman A and Aalbers MB (2016) London and New York as a safe deposit box for the transnational wealth elite. Environment and Planning A48(12):2443–2461

FFA Private Bank (2011) The Lebanese Banking Sector: August 2011. Beirut: FFA Private Bank

Finger H and Hesse H (2009) Lebanon—Determinants of commercial bank deposits in a regional financial center. IMF Working Paper WP/09/195. International Monetary Fund

Gaspard TK (2004) A Political Economy of Lebanon, 1948–2002. The Limits of Laissez-Faire.Leiden/Boston: Brill

Gates C (1998) The Merchant Republic of Lebanon: Rise of an Open Economy. London: Centre for Lebanese Studies/I.B. Tauris

Gberie L (2002) War and Peace in Sierra Leone: Diamonds, corruption and the Lebanese connection. The Diamonds and Human Security Project, Occasional Paper #6

Gebara H, Khechen M and Marot B (2016) Mapping New Constructions in Beirut (2000–2013).Jadaliyya. www.jadaliyya.com/pages/index/25504/mapping-new-constructions-in-beirut-(2000–2013) (last accessed 21 November 2016)

Global Property Guide (2011) Lebanon’s residential price rises have continued. October issue, Global Property Guide

Gotham KF (2009) Creating liquidity out of spatial fixity: The secondary circuit of capital and the subprime mortgage crisis. International Journal of Urban and Regional Research33(2):355–371

Grant R (2007) Geographies of investment: How do the wealthy build new houses in Accra, Ghana? Urban Forum18(1):31–59

Habib O (2014) Housing institute receives cash from treasury. The Daily Star1 August

Halawi D (2010) Non-residents buying bulk of Lebanese real estate. The Daily Star17 April

Hanieh A (2011) Capitalism and Class in the Gulf Arab States. Houndmills/Basingstoke/Hampshire: Palgrave Macmillan

Hanieh A (2016) Absent regions: Spaces of financialisation in the Arab world. Antipode48(5):1228–1248

Hardie I (2012) Financialization and Government Borrowing Capacity in Emerging Markets. Houndmills/Basingstoke/Hampshire: Palgrave Macmillan

Harvey D (1978) The urban process under capitalism: A framework for analysis. International Journal of Urban and Regional Research2(1–4):101–131

Harvey D (2001) Globalization and the “spatial fix.” Geographische Revue 3(2): 23–30

Harvey D (2010) The Enigma of Capital and the Crises of Capitalism. New York: Oxford University Press

Hertog S (2007) The GCC and Arab economic integration: A new paradigm. Middle East Policy, 14(1):52–68

Hourani G (2009) The global financial crisis: Impact on Lebanese expatriates in the Gulf. Center for Migration and Refugee Studies, The American University in Cairo, Working Paper. http://www.aucegypt.edu/GAPP/cmrs/reports/Documents/HOURANI.pdf (last accessed 9 January 2014)

Hourani G (2010) Lebanese migration to the Gulf (1950–2009). Middle East Institute Viewpoints(pp 9–12). http://www.mei.edu/Portals/0/Publications/Migration%20Mashreq.pdf (last accessed 14 October 2015)

Hourani G (2014) Bilateral relations, security and migration: Lebanese expatriates in the Gulf States. European Scientific Journal1:643–657

Hourani NB (2010) Transnational pathways and politico-economic power: Globalisation and the Lebanese Civil War. Geopolitics15(2):290–311

Hourani NB (2013) Lebanon: Hybrid sovereignties and U.S. foreign policy. Middle East Policy20(1):39–55

Johnson S (2017) Lebanon defies odds to keep its finances afloat. The Daily Star12 June

Kanj O and Khoury R El (2013) Determinants of non-resident deposits in commercial banks: Empirical evidence from Lebanon. International Journal of Economics and Finance5(12):135–150

Karam Z (2010) Luxury building boom transforms Beirut as Lebanon becomes a financial draw. Associated Press22 January

Khalaf S and Kongstadt P (1973) Hamra of Beirut: A Case of Rapid Urbanization. Leiden: F.J. Brill

Khoury R El and Kanj O (2013) Determinants of deposits in Lebanese commercial banks: Evidence from non-resident depositors. Journal of Money, Investment and Banking(27):151–168

Krijnen M (2010) Facilitating real estate development in Beirut: A peculiar case of neoliberal public policy. MA-thesis, American University of Beirut

Krijnen M (2016) The urban transformation of Beirut. An investigation into the movement of capital. PhD-thesis, Ghent University

Krijnen M (2018) Beirut and the creation of the rent gap. Urban Geography 39(7):1041–1059

Krijnen M and De Beukelaer C (2015) Capital, state and conflict: The various drivers of diverse gentrification processes in Beirut, Lebanon. In: L Lees, HB Shin and E López-Morales (eds) Global Gentrifications: Uneven Development and Displacement (pp 285–309). Bristol and Chicago: Policy Press

Krijnen M and Fawaz M (2010) Exception as the rule: High-end developments in neoliberal Beirut. Built Environment36(2):245–259

Krijnen M, Bassens D and van Meeteren M (2017) Manning circuits of value: Lebanese professionals and expatriate world-city formation in Beirut. Environment and Planning A 49(12):2878–2896

Kubursi AA (1999) Reconstructing the economy of Lebanon. Arab Studies Quarterly21(1):69–95

Kutz W and Lenhardt J (2016) “Where to put the spare cash?” Subprime urbanization and the geographies of the financial crisis in the Global South. Urban Geography37(6):926–948

Labaki B (2006) The role of transnational communities in fostering development in countries of origin. The case of Lebanon.Working Paper, UN/POP/EGM/2006/13. Beirut: ESCWA

Maalo D (2010) Lebanon’s banks keep crisis at bay. The Banker. http://www.thebanker.com/news/fullstory.php/aid/7328/Lebanon_s_banks_keep_crisis_at _bay.html? current_page=NO_PAGE (last accessed 6 February 2017)

Marot B (2014) The end of rent control in Lebanon: Another boost to the “growth machine?” Jadaliyya. http://www.jadaliyya.com/pages/index/18093/the-end-of-rent-control-in-lebanon_another-boost-t (last accessed 15 March 2015)

McGinley S (2010) Alarm raised on Beirut property bubble. October issue, Arabian Business

Musa MAN (2013) Constructing global Amman: Petrodollars, identity, and the built environment in the early twenty-first century. PhD-thesis, University of Illinois at Urbana-Champaign

Nash M (2014) Taking their time. Developers plot their next moves while the market is slow. July issue, The Executive

Nasr S (1978) Backdrop to civil war: The crisis of Lebanese capitalism. MERIP Reports73:3–13

Pearlman W (2014) Competing for Lebanon’s diaspora: Transnationalism and domestic struggles in a weak state. International Migration Review48(1):34–75

Peters D, Raad E and Sinkey JF (2004) The performance of banks in post-war Lebanon. International Journal of Business9(3):259–286

“Plus de 300 chantiers résidentiels à Beyrouth” (2009) L’Orient Le Jour29 October

Rouanet H and Halbert L (2014) Leveraging finance capital: Urban change and self-empowerment of real estate developers in India. Urban Studies53(7):1401–1423

Saad W (2014) Financial development and economic growth: Evidence from Lebanon. International Journal of Economics and Finance6(8):173–186

Sadikov A, Kyobe A, Nakhle N, et al. (2012) Lebanon: Selected issues. IMF Country Report, Washington D.C.

Sakr E (2013) Central Bank package to revitalize real estate. The Daily Star5 February

Schellen T (2013) Lending homeowners a hand. BDL subsidies favor those who can afford the down payment. April issue, The Executive

Shwayri ST (2008) From regional node to backwater and back to uncertainty: Beirut 1923–2006. In: Y Elsheshtawy (ed) The Evolving Arab City: Tradition, Modernity and Urban Development (pp 69–98).London: Routledge

Silver BJ (2003) Forces of Labor. Workers’ Movements and Globalization Since 1870. New York: Cambridge University Press

Simpson T (2013) Scintillant cities: Glass architecture, finance capital, and the fictions of Macau’s enclave urbanism. Theory, Culture & Society30(7–8):343–371

Smith N (1984) Uneven Development. Nature, Capital, and the Production of Space. 2nd ed. Oxford and Cambridge: Basil Blackwell

Smith N (1986) Gentrification, the frontier and the restructuring of urban space. In: N Smith and P Williams (eds) Gentrification of the City (pp 15–34). Abingdon & New York: Routledge

Srouji S (2005) Capturing the state: A political economy of Lebanon’s public debt crisis 1992–2004. MA-thesis, Institute of Social Studies

The World Bank (2012) Using Lebanon’s large capital inflows to foster sustainable long-term growth. Report No. 65994-LB. Beirut: The World Bank

Traboulsi F (2014) Social Classes and Political Power in Lebanon. Beirut: Heinrich Böll Stiftung

UN-Habitat and UNHCR (2014) Housing, Land and Property in Lebanon: Implications of the Syrian Refugee Crisis. Fawaz M, Saghiyeh N, and Nammour K (eds). Beirut: UN-Habitat

Wehbe M (2014a) Beirut for the rich only: An average of $1m for a residential apartment. Al Akhbar English14 February

Wehbe M (2014b) Lebanese banks in 2013: Profits and their sources. Al Akhbar English15 February

Wehbe M (2014c) Liberalizing the rent market: Real estate speculators to evict both tenants and landlords. Al Akhbar English8 June

Wu CT (2000) Diaspora capital and Asia Pacific urban development. In: G Bridge and S Watson (eds) A Companion to the City (pp 207–223). Oxford, UK: Blackwell Publishing

Wyly, EK Atia M and Hammel DJ (2004) Has mortgage capital found an inner‐city spatial fix? Housing Policy Debate15(3):623–685

[1]Cement deliveries normally happen when a project is already under construction, i.e. after investment has been planned and partially carried out. Construction permits are usually delivered six months to two years after a project is planned (Krijnen 2010), when projects have already started to sell or might not actually be under construction at all. These indicators are moreover only available on a nationwide scale, even though most investments were directed to Beirut. As for the real estate transactions, which pertain to Beirut, not all are registered at the Land Registry right away; buyers can wait ten years to register (Bou Akar 2005), although registration is usually required in order to obtain a housing loan.

[2]I use the term expatriate workers instead of diaspora members, because the majority of expatriates holds on to its Lebanese nationality and maintains strong ties with the home country, aiming to return.

[3]The exact nature of capital flows cannot be determined because of Lebanon’s banking secret and because numbers on Foreign Direct Investment in real estate do not accurately reflect investments by Lebanese expatriates. See also The World Bank (2012). It is probably also possible to identify a third category of capital flows, originating in illegitimate activities such as the drug and arms trade (Dillman 2007), illegal diamond mining, and other forms of organized crime. Many observers state that Beirut’s built environment provided the perfect means through which to launder illegal or criminal money. I have been unable to confirm this due to the lack of data on such operations and the sensitive nature of the topic. However, it is certainly plausible that for example some money originates from the diamond industry in Sierra Leone, since this industry is dominated by Lebanese (see Gberie 2002). Traboulsi (2014:94) discusses a case of a bank laundering money for the Russian mafia, Saudi Arabian Islamist groups and Saddam Hussein’s regime, mostly through real estate.

[4]Harvey (1978) prefers the term “productive” to “profitable” for several reasons, including the risk of treating the total profit as the total surplus value. He defines a “productive” investment as “one which expands the basis for the production of surplus value” (Harvey 1978:110).

[5]The state’s focus on facilitating the tertiary sector came at the expense of industrialization and social welfare; Lebanon’s ruling elites were traditionally closely linked to banking and finance and did not employ any postcolonial nationalist or redistributive policies, like Egypt or Syria had done (Gates 1998). Naturally, a large number of Lebanon’s citizens were left behind in abject poverty, and this, together with unfavorable geopolitical circumstances, ultimately led to the destruction of the “Switzerland of the Middle East.” The country descended into civil war when conflicting stakes regarding social welfare, pan-Arabism and the role of the Palestinian resistance in Lebanon could not be accommodated peacefully.

[6]Interview with the vice-president of an economic think tank, December 10, 2013.

[7]Interview with the director of an advertising agency, December 10, 2014.

[8]The US government has since indicted Ahmad and some of his partners for defrauding them during projects in Iraq, see http://www.fbi.gov/albuquerque/press-releases/2012/former-officers-of-new-mexico-based-defense-contractor-charged-in-fraud-and-money-laundering-schemes-related-to-rebuilding-efforts-in-iraq.

[9]Interview with a board member of REDAL, October 21, 2014. REDAL stands for the Real Estate Developers Association Lebanon. See http://www.redal.org.lb for more information.

[10]Interview with sales representative, April 30, 2012.

[11]In 2007, Central Bank governor Riad Salameh issued directives that prevented Lebanese banks from engaging in risky speculation: ‘The most significant measures include banks not being allowed to take on too much debt, having to have at least 30% of their assets in cash and being forbidden from speculating in risky packages of bundled-up debts—precisely the root cause of the financial crisis’ (Maalo 2010).

[12]While banking secrecy has come under fire since 9/11, when US authorities started a crackdown on tax evasion and alleged terrorism financing worldwide, Lebanon has managed to stay off the blacklist while keeping most of its banking secrecy in place. It is only to be lifted in suspicious cases, according to new laws passed in December 2015.

[13]Interview with the vice-president of an economic think tank, December 10, 2013.

[14]Interview with an economy professor, March 11, 2015. This suspicion was confirmed by a finance consultant, interviewed March 11, 2015.

[15]Interview with a finance journalist, October 15, 2014.

[16]For example, MENA Capital, one of the largest real estate developers in Lebanon, canceled their planned gated community in the Corniche en-Nahr area (Krijnen 2016).

[17]According to data provided by the Central Bank, see http://www.bdl.gov.lb/webroot/statistics/ table.php?name=t5271-3.

[18]Interview with an economic researcher, October 10, 2014.

[19]Interview with board member of REDAL (Real Estate Developers Association Lebanon), December 12, 2013.

[20]See, for example propertyfinder.com.lb, which offers a mortgage calculator as well, or http://www.bnooki.com/housing-loans-lebanon (last accessed September 17, 2014).

[21]I would like to thank Michiel van Meeteren for pointing me towards Silver (2003).